what is supposed to happen in april 2018

Mortgage rate forecast for next week (April eleven-15 )

With inflation in high gear and the Federal Reserve planning six more hikes this yr, it'south been full steam ahead for mortgage rates.

The average xxx-year fixed interest rate spiked again, going from iv.42% on March 24 to four.67% on March 31. Information technology marked the highest boilerplate since December. 2018.

Most involvement rate indicators continue to point up, although a new Covid outbreak or the war in Ukraine condign more unstable could cause a curt-term decline.

In this article (Skip to...)

- Will rates get downwards in Apr?

- 90-day forecast

- Expert rate predictions

- Mortgage rate trends

- Rates past loan type

- Mortgage strategies for Apr

- Mortgage rates FAQ

>Related: Cash-out refinance: Best uses for your habitation equity

Will mortgage rates get down in Apr?

Mortgage rates saw celebrated growth to commencement 2022, surging over 145 basis points (i.45%) through the starting time quarter.

With aggrandizement at 40-year highs, the pandemic'south economic touch subsiding and the Federal Reserve outlining its 2022 policy plan, this could simply be the beginning.

Experts from Fannie Mae, NAR, Redfin, and other industry leaders think 30-year mortgage rates could go as loftier equally 4.5% in April. And none expect them to stay below iv% for any sustained period.

Of course, the war in Europe or a spike from a new Covid variant could cause involvement rates to fall or add together variance.

"Information technology wouldn't shock me if we laissez passer iv.25% or even get to 4.v% this month, depending on how the market starts pricing in what the Fed says."

—Doug Duncan, SVP and master economist at Fannie Mae

Doug Duncan, SVP and principal economist at Fannie Mae

Prediction: Rates will rising

"The path is going to be upwards. How much depends on a whole bunch of factors. The Fed signaled they're going to enhance [its fed funds rate target] every time they see this twelvemonth.

Now there'southward chatter about whether the Fed will be even more aggressive and exercise a fifty footing point increase at the next coming together. It's also not unreasonable to recollect they might practise a 50 basis point increase and so not practise one in the fall as they're watching the runoff of the portfolio.

But it wouldn't shock me if we pass 4.25% or fifty-fifty become to 4.five% this month, depending on how the marketplace starts pricing in what the Fed says. The key will be the release of the [FOMC March] minutes, which come up out three weeks afterwards the meeting. Powell specifically told reporters go look at the minutes because they volition contain details on the runoff of the portfolio. When those minutes come out, I would look there to be some sort of market reaction."

Nadia Evangelou , senior economist and director of forecasting at National Association of Realtors

Prediction: Rates will rising

"While the next few weeks will be unpredictable as markets go on to churn, the outlook is for mortgage rates to rise fifty-fifty higher. The Federal Reserve indicated six more interest rate increases past the end of the twelvemonth. Even so, inflation will eventually start slowing downwardly quondam afterward this year.

The Federal Reserve forecasts inflation to average 4.3% in 2022. Thus, I wait some of this affect to be mitigated eventually through lower aggrandizement. I forecast mortgage rates to average around 4.4% at the terminate of the year.

Mortgage rates will probable hover effectually iv.two% in April. Inflation will continue to remain elevated while college short-term interest rates volition put upwards pressure level on mortgage rates side by side month."

Selma Hepp , deputy chief economist at CoreLogic

Prediction: Rates will vary

"While the rates are probable to be higher by the finish of the year, the path of the increment is less certain.

There has already been a notable jump in rates in recent weeks equally a issue of the disharmonize in Ukraine and the FOMC declaration. All the same, some of that increment may subside given the widening spread between mortgage rates and treasuries."

Joel Kan , associate vice president, industry surveys and forecasts at Mortgage Bankers Clan

Prediction: Rates will rise

"Our economical outlook reflects the potential for slower but still stable economic growth and a healthy task marketplace. The economy remains strong just a renewed bout of supply-chain constraints and disruptions stemming from the war in Ukraine is likely to push aggrandizement higher.

"MBA forecasts that mortgage rates will rising further over the next year to around 4.v%. Mortgage rates take been exceptionally volatile in contempo weeks, given the profound uncertainties both with respect to the geopolitical situation and monetary policy. Hopefully, the Fed's actions of raising its short-term rate target for the beginning time since 2018 and explanations can help to reduce the policy uncertainty and rate volatility."

Odeta Kushi , deputy chief economist at Beginning American

Prediction: Rates will rising

"Mortgage rates are notoriously difficult to forecast considering they're tied to the wider economy and global geopolitical events. The ongoing Russia-Ukraine conflict continues to insert an element of incertitude into fiscal markets, which could result in downward pressure on mortgage rates.

Merely the general expectation is that mortgage rates are trending upwards and take already increased based on the expectation of the Fed tightening budgetary policy this year.

Expect mortgage rates to go on to rise in April, merely nosotros could come across some week-to-week volatility every bit Fed tightening, among other factors, propels rates frontward, while geopolitical doubt may ballast rates temporarily."

Taylor Marr , deputy chief economist at Redfin

Prediction: Rates will rise

"Redfin's expectation is that rates will continue to rising steadily through April — to perhaps 4.4% by the cease of the month. This will happen as investors await the Fed to put upward force per unit area on mortgage rates via winding down their roughly $9 trillion balance sheet of both treasuries and mortgage backed securities in 2022.

Information technology'southward worth noting that Jerome Powell said this calendar week that they could brainstorm that process equally early as May, just more details will be released in the Federal Open Market Committee minutes in early Apr. While at that place may be global events that could counteract this ascent, such equally the war in Eastern Europe and new variants of COVID-19 spreading in Asia, the probable flick is that we won't run into rates under four% anymore. The take chances of rates increasing 20-30 footing points by the end of April is only growing."

Rick Sharga , executive vice president at RealtyTrac

Prediction: Rates will ascent

"Inflation, Fed actions, and rise yields on U.Due south. Treasuries all bespeak towards mortgage rates increasing in April.

Inflation is unlikely to come down in the short term, as energy prices continue to ascent and we're probable to run into more supply chain disruption due to a new widespread COVID-19 outbreak in Communist china and Russian federation'due south invasion of Ukraine.

And somewhat surprisingly, rates on the x-Yr U.S. Treasury in mid-March hit their highest betoken since June of 2019 at 2.187%. This increase runs counter to the notion that a "flight to rubber" during volatile times would bulldoze treasury prices up and yields downwardly. And since there's usually most a two-point spread between Treasury yields and 30-year mortgage rates, that suggests we could see mortgage rates as high every bit iv.0%-iv.25% during April."

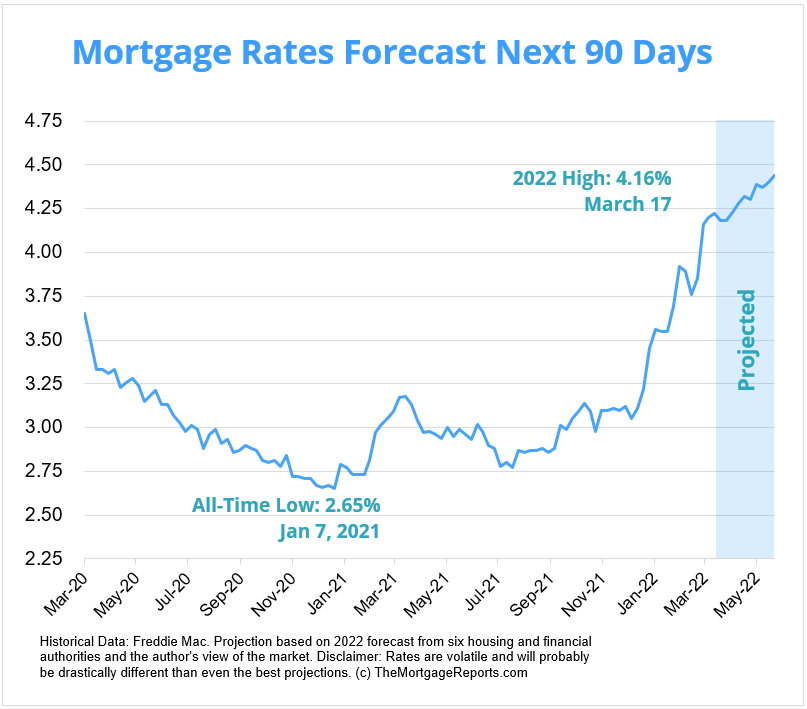

Mortgage interest rates forecast next 90 days

Aside from the Russian-Ukrainian conflict'southward uncertainty or the next wave of Covid bringing dorsum restrictions, all other major indicators signal to mortgage rate growth.

The about likely outcome will be average interest rates on an overall uptrend in the next three months. Of form, they have high volatility and rarely go in a straight line from week to week so nosotros could run into some drops mixed in also.

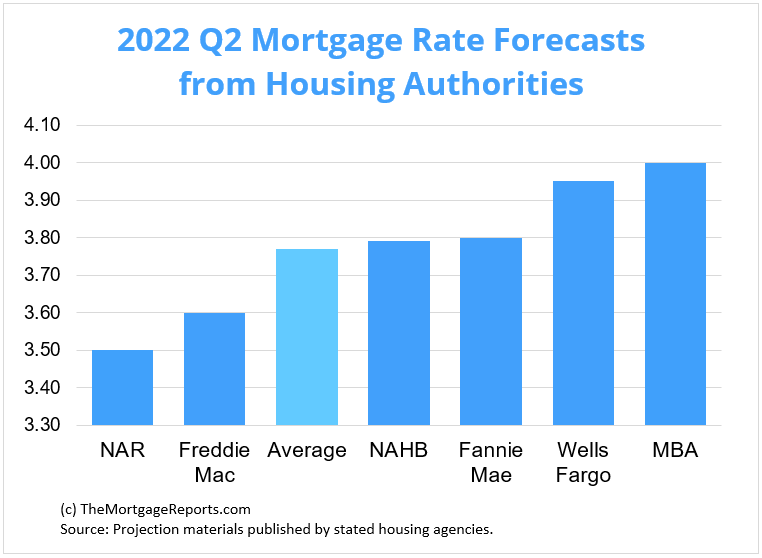

Mortgage charge per unit predictions for 2022

The average 30-year fixed rate mortgage concluded 2021 at 3.i%, according to Freddie Mac.

All six of the major housing authorities we gathered project that boilerplate to rise over the second quarter of 2022.

The National Association of Realtors and Freddie Mac sit at the low end of the group, estimating the average xxx–year fixed interest rate to settle at 3.5% or iii.half-dozen% by the end of Q2. Wells Fargo and the Mortgage Bankers Association had the highest predictions, with forecasts of three.9% and 4.0%, respectively, by the end of June.

| Housing Dominance | xxx-Year Mortgage Rate Forecast (Q2 2022) |

| National Association of Realtors | three.l% |

| Freddie Mac | 3.60% |

| National Association of Domicile Builders | three.79% |

| Fannie Mae | 3.fourscore% |

| Wells Fargo | 3.90% |

| Mortgage Bankers Clan | 4.00% |

| Average Prediction | iii.77% |

Electric current mortgage involvement rate trends

Mortgage rates took another huge leap this by week, with the average ballooning 25 basis points (0.25%).

The boilerplate 30-year fixed charge per unit grew from four.42% to four.67% for the seven days ending March 31, according to Freddie Mac's weekly rate survey.

Similarly, the 15–year stock-still rate increased from 3.63% to three.83%, while the average rate for a 5/1 ARM rose from iii.36% to 3.50%.

| Month | Average 30-Year Fixed Rate |

| March 2021 | three.08% |

| Apr 2021 | 3.06% |

| May 2021 | 2.96% |

| June 2021 | 2.98% |

| July 2021 | two.87% |

| August 2021 | 2.84% |

| September 2021 | 2.90% |

| October 2021 | 3.07% |

| November 2021 | 3.07% |

| December 2021 | three.10% |

| January 2022 | 3.45% |

| Feb 2022 | three.76% |

Source: Freddie Mac

Mortgage rates are moving away from the record–depression territory seen in 2020 and 2021 but are nonetheless low from a historical perspective.

Dating back to April 1971, the fixed xxx–year interest charge per unit averaged 7.79%, according to Freddie Mac.

So if you haven't locked a rate yet, don't lose too much sleep over it. Yous tin can still get a bang-up deal — peculiarly for borrowers with strong credit.

Just make certain you shop effectually to find the all-time lender and everyman charge per unit for your unique state of affairs.

Mortgage charge per unit trends by loan type

Many mortgage shoppers don't realize in that location are different types of rates in today's mortgage market place.

But this knowledge can help abode buyers and refinancing households discover the best value for their situation.

Following are 3-month mortgage rate trends for the most popular types of domicile loans: conventional, FHA, VA, and jumbo.

| February 2022 | Jan 2022 | December 2021 | |

| Conforming Loan Rates | 4.09% | 3.77% | three.35% |

| FHA Loan Rates | 4.11% | 3.86% | iii.45% |

| VA Loan Rates | iii.77% | 3.56% | 3.02% |

| Jumbo Loan Rates | three.76% | iii.45% | 3.23% |

Source: Blackness Knight Originations Market Monitor Study

Which mortgage loan is best?

The best mortgage for you depends on your financial situation and your goals.

For instance, if you want to purchase a high-priced home and you accept cracking credit, a jumbo loan is your best bet. Jumbo mortgages allow loan amounts above befitting loan limits — which max out at $647,200 in most parts of the U.South.

On the other hand, if you're a veteran or service member, a VA loan is almost e'er the right choice.

VA loans are backed by the U.S. Section of Veterans Affairs. They provide ultra-depression rates and never charge private mortgage insurance (PMI). Simply you need an eligible service history to authorize.

Conforming loans and FHA loans (those backed by the Federal Housing Administration) are smashing low-down-payment options.

Conforming loans let every bit little every bit 3% downwardly with FICO scores starting at 620.

FHA loans are even more lenient well-nigh credit; home buyers can oftentimes qualify with a score of 580 or higher, and a less-than-perfect credit history might not disqualify you.

Finally, consider a USDA loan if you lot want to buy or refinance existent manor in a rural area. USDA loans accept below-market rates — similar to VA — and reduced mortgage insurance costs. The catch? You lot demand to live in a 'rural' expanse and have moderate or low income to be USDA-eligible.

Mortgage charge per unit strategies for Apr 2022

Mortgage rates started 2022 with large growth — a trend that'southward expected to go along in April and over the residual of the year. Just opportunities to lock in a low involvement rate do still exist for dwelling house buyers and refinancing homeowners.

Hither are but a few strategies to keep in heed if you're mortgage shopping in the next few months.

Make a move before the next FOMC meeting

The Federal Reserve made its 2022 plans very clear; information technology will enhance the target range on its federal funds rate after each of the twelvemonth'south remaining six FOMC meetings.

It's a move the Fed makes in order to combat inflation, and mortgage rates almost always grow in correlation.

Interest rates jumped after both FOMC meetings so far this year, with a 31 basis point (0.31%) surge to the average 30-year fixed charge per unit immediately following March's meeting.

While mortgage rates are famously volatile and many factors can cause a weekly subtract, nearly every indicator points to them growing over the course of the year.

If you lot're in the market for a new home loan or a refinance — and tin beget to — the best time to lock in a charge per unit, in all likelihood, is correct now. And remember, preparation is cardinal and then go all your paperwork organized and done before consulting with a lender.

Always stir competition

Interest rates are on the rise and are expected to go on going upwards in 2022.

The all-time way to get a proficient bargain — especially now that rates no longer sit down near all-time lows — is to make lenders compete for your concern.

Getting a qualified or prequalified rate from a lender is the showtime step. Then, shop that rate around to other lenders and see if any of them volition offer you a improve one.

Driving competition between multiple mortgage companies is how many people terminate upwards with lower rates and save money over the life of their loan. And why wouldn't you want to salvage coin?

How to compare interest rates

Rate shopping doesn't just mean looking at the lowest rates advertised online considering those aren't available to everyone. Typically, those are offered to borrowers with perfect credit and who can put a downwards payment of twenty% or more.

The rate lenders really offering depends on:

- Your credit score and credit history

- Your personal finances

- Your down payment (if ownership a domicile)

- Your abode equity (if refinancing)

- Your loan-to-value ratio (LTV)

- Your debt-to-income ratio (DTI)

To figure out what rate a lender can offer you based on those factors, you have to make full out a loan application. Lenders will cheque your credit and verify your income and debts, and so give you a 'real' rate quote based on your fiscal state of affairs.

You should get 3-5 of these quotes at a minimum. Then compare them to notice the all-time offer.

Look for the lowest rate, but also pay attention to your annual pct rate (APR), estimated closing costs, and 'disbelieve points' — extra fees charged upfront to lower your charge per unit.

This might sound similar a lot of piece of work. Only you lot can store for mortgage rates in under a mean solar day if yous put your heed to it. And shaving just a few footing points off your charge per unit can save you lot thousands.

Mortgage interest charge per unit FAQ

What are electric current mortgage rates?

Current mortgage rates are averaging 4.67% for a 30–year fixed–rate loan, iii.83% for a 15–year fixed–rate loan, and 3.50% for a v/one adjustable–rate mortgage, according to Freddie Mac's latest weekly charge per unit survey. Your individual charge per unit could be higher or lower than the average depending on your credit score, down payment, and the lender you choose to work with, among other factors.

Will mortgage rates get down next week?

Mortgage rates could subtract next week (April 11-15, 2022) depending on how the war in the Ukraine progresses. Though rates could ascent if strong aggrandizement continues and the market place adjusts to Federal Reserve'due south rate hikes.

Will mortgage interest rates become down in 2022?

It'due south unlikely mortgage rates will go down in 2022. Inflation has been climbing at a tape rate over the last few months. And the Fed is planning to raise interest rates later each of its scheduled FOMC meetings. Both these factors should lead to significantly higher mortgage rates in 2022.

Will mortgage involvement rates go up in 2022?

Yes, it'south very probable mortgage rates will increase in 2022. High aggrandizement, a strong housing marketplace, and policy changes past the Federal Reserve should all push rates higher in 2022. The merely thing likely to push rates down would be a major resurgence in serious Covid cases and further economical shutdowns. But, while information technology could assistance mortgage rates, no one is hoping for that outcome.

What is the everyman mortgage charge per unit correct now?

Freddie Mac is now citing average xxx–year rates in the high-3 to low-4 percent range. But remember that rates vary a lot by borrower. Those with perfect credit and large downward payments may get below–boilerplate involvement rates, while poor–credit borrowers and those with non–QM loans could see much higher rates. Yous'll need to get pre–approved for a mortgage to know your verbal rate.

Will there exist a housing crash in 2022?

For the most role, industry experts do not expect the housing marketplace to crash in 2022. Yeah, home prices are over–inflated. But many of the risk factors that led to the 2008 crash are not present in today's market. Low inventory and massive buyer demand should keep the market propped upward next year. Plus, mortgage lending practices are much safer than they used to exist. That means there's not a subprime mortgage crisis waiting in the wings.

What is the lowest mortgage charge per unit ever?

At the fourth dimension of this writing, the lowest 30–year mortgage rate ever was 2.65 percent. That's according to Freddie Mac'southward Main Mortgage Market Survey, the virtually widely–used benchmark for current mortgage involvement rates.

Should I lock my rate now or wait?

Locking your charge per unit is a personal determination. You lot should do what's right for your situation rather than trying to time the market. If yous're buying a abode, the right time to lock a charge per unit is after y'all've secured a purchase understanding and shopped for your best mortgage deal. If you're refinancing, you should make sure yous compare offers from at least three to v lenders before locking a rate. That said, rates are ascent. So the sooner you can lock in today'south market, the meliorate.

Is now a good time to refinance?

That depends on your situation. It'southward a practiced fourth dimension to refinance if your current mortgage rate is above market rates and you could lower your monthly mortgage payment. Information technology might also exist good to refinance if you can switch from an adaptable–rate mortgage to a low fixed–charge per unit mortgage; refinance to get rid of FHA mortgage insurance; or switch to a brusque–term ten– or xv–twelvemonth mortgage to pay off your loan early.

Is it worth refinancing for 1 percentage?

It'due south oftentimes worth refinancing for 1 per centum point, as this can yield significant savings on your mortgage payments and total involvement payments. Only make sure your refinance savings justify your closing costs. Y'all can use a mortgage calculator or speak with a loan officer to crunch the numbers.

How do I store for mortgage rates?

Start by choosing a list of 3–5 mortgage lenders that you're interested in. Expect for lenders with low advertised rates, great customer service scores, and recommendations from friends, family, or a real estate amanuensis. Then go pre–approved by those lenders to encounter what rates and fees they can offer yous. Compare your offers (Loan Estimates) to find the best overall deal for the loan type y'all desire.

What are today's mortgage rates?

Low mortgage rates are still available. Connect with a mortgage lender to find out exactly what charge per unit yous qualify for.

iToday's mortgage rates are based on a daily survey of select lending partners of The Mortgage Reports. Interest rates shown hither assume a credit score of 740. Meet our full loan assumptions here.

Selected sources:

- https://www.blackknightinc.com/category/press-releases

- https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm

- http://www.freddiemac.com/research/datasets/refinance-stats/alphabetize.page

The information contained on The Mortgage Reports website is for informational purposes simply and is not an advertizing for products offered by Full Beaker. The views and opinions expressed herein are those of the author and do not reflect the policy or position of Total Beaker, its officers, parent, or affiliates.

Source: https://themortgagereports.com/32667/mortgage-rates-forecast-fha-va-usda-conventional

0 Response to "what is supposed to happen in april 2018"

Post a Comment